ICOs are Cancer

The Problem

ICOs misguidedly attempt to solve four perceived problems in the market:

- Government regulations designed to protect poor people from making risky investments have ended up allowing only the rich to participate in some of the most lucrative investments. The way the government views things, if you have less than $1MM you are not an “accredited investor” and can’t be trusted to make important financial decisions on your own behalf.

- Access to liquidity for early investors. When you invest in a startup, even in the best case scenario it takes many years before you’ll ever see a penny of your investment returned. VC funds typically have 8+ year time horizons.

- More investment for startups. Starting a company is hard. Isn’t a tool that allows more connections between investors and startups only a good thing?

- Platform profit-sharing (utility tokens). If you were an early user who helped contribute to the success of a social network like Facebook/Twitter/Instagram/WhatsApp/Reddit/etc, then you receive no extra compensation for helping that company achieve success.

#1 is a real problem that blockchains don’t solve, #2 exists for good reasons (that are naturally mitigated by market forces without ICOs), and #3 and #4 are edge cases that create more problems than they solve.

#1 Government Regulation

US investment regulations have run amok. It’s strange that the government runs ads on TV encouraging you to buy their lottery tickets but also (mostly) bans you from investing in high risk/reward activities like venture capital. There is a legitimate fear of your grandparents being swindled by a slick salesman out of their retirement, but the current regulations are blunt, arbitrary, and ineffective. They also make it hard for foreigners to invest in American startups, which only hurts Americans. That said, the solution here is for the US government to get out of the way. One thing I’m thankful to ICOs for is that they’ve given a counterpoint to regulators’ “control everything” mindset, now that we can see the damage caused by pushing some legitimate companies towards ICOs.

Regardless of whether you think these government regulations are making the world better or worse, ICOs don’t actually avoid these regulations at all! The whole reason Satoshi Nakamoto invented the blockchain (and hid behind a pseudonym) was to create something that was censorship resistant against third parties and state actors. What’s unique about bitcoin (vs other tokens) is the highly decentralized nature. Unless the project whose token you bought is 100% anonymous (no known principals) and doesn’t have a bank account, then there is a single point of failure where the government can easily exert pressure if they disagree with what that project is doing (for example, not following securities laws). Once they go after a project, the value of that token will plummet. Just ask the founders of Liberty Reserve how that worked out for them and their investors.

In case you think the government’s stance on these is ambiguous, check out what current and former SEC regulators have to say:

Using a blockchain without a need for censorship resistance is like using a rube goldberg machine to turn the page on your newspaper:

#2 Access to Liquidity

Venture capital investments are unusual in that even the most successful investments often return little-to-no capital to their early investors for many years.

There is good reason for this: building a billion dollar company is a massive undertaking, and investors (and employees) should have a very long-term time horizon to accomplish such audacious goals. Would you buy stock in a company if the senior management was dumping that stock? Investment structures that require incentive alignment are essential to discourage bad behavior. Typically, insiders (including early investors) are restricted from selling equity immediate before or after an IPO so that outsiders are treated fairly.

That said, there are still ways to get some liquidity. Here is famous Venture Capitalist Fred Wilson of Union Square Ventures describing how their firm sold stock in Twitter and a host of other companies well before their IPO (source):

We have done similar things in many other situations including Zynga, Lending Club, MongoDB, and a number of other investments. We typically seek to liquidate somewhere between 10% and 30% of our position in these pre-IPO liquidity transactions. Doing so allows us to hold onto the balance while de-risking the entire investment.

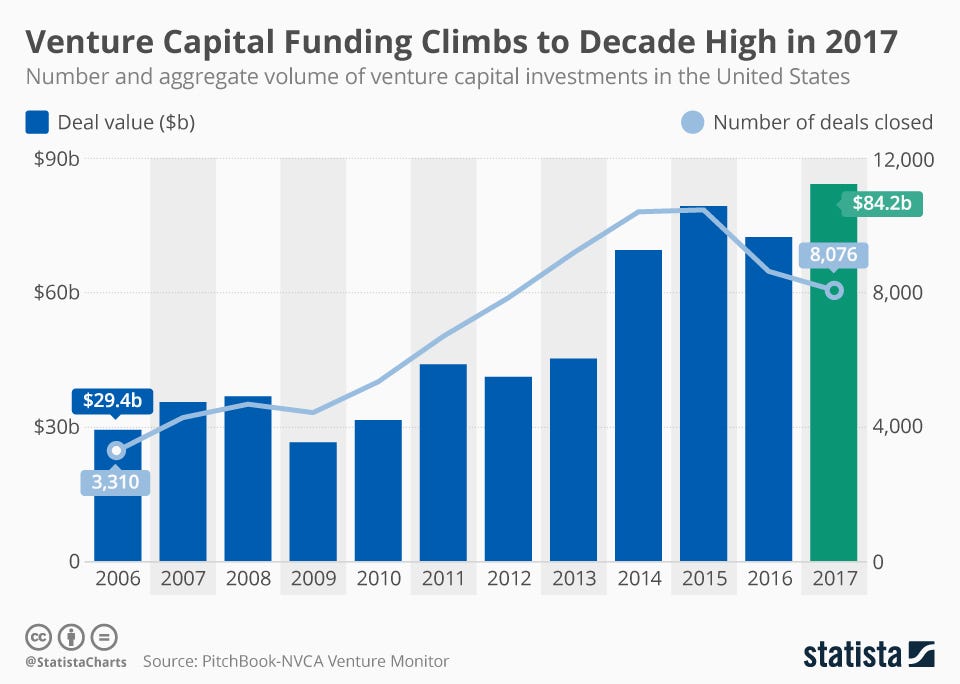

#3 More Investment for Startups

It is certainly amazing that teams are able to raise tens of millions of dollars from investors all over the world, but is this a problem without ICOs?

It turns out, that more money has been pouring into the space (and at more favorable prices for founders) for a long time:

While some will complain that it’s hard to raise money, given how easy it is for so many it’s difficult to take claims from these “wantrapreneurs” seriously.

Before you argue that tokens will bypass the VC industry and allow individuals to back other individuals, keep in mind that actual ICO investors are often just a small group of wealthy VCs.

There is perhaps room for a notable exception for non-US startups, which have historically done quite poorly as the US has by far the most investors and startup infrastructure. The most relentless founders have traditionally been able to move across the world to increase their chances at success. That will probably not hold forever, but even then you’d be better off to make an investment directly on a foreign company’s cap table than in their token.

#4 Platform Profit-Sharing (aka “Utility Tokens”)

In a business with strong network-effects, utility tokens could incentivize a group of users to evangelize a platform and help it reach critical mass. That part actually makes sense. There is a reason why nearly all publicly traded companies have Employee Stock Purchase Plans (ESPPs); utility tokens have extended that model to customers (with different interests).

When you look at these utility tokens more closely, there’s no logical reason for them to achieve monetary status in the long run:

- Most companies are not actually platforms with powerful network effects, so the value added by the early users doesn’t justify granting them ownership in the company. Remember that the users are signing up voluntarily (and sometimes paying money for the privilege), meaning they already believe in the benefits of the service.

- It becomes very hard to pivot or make adjustments if the model you built your utility token around doesn’t work. You have too many stakeholders and it wouldn’t be fair to change the economics that they had agreed to if you decided for example to launch another product that didn’t have use for the token. It would also crash your utility token’s price, similar to the way managers of publicly traded companies optimize for quarterly results over the long-term health of the company.

- Designing a cryptocurrency protocol is enormously complex and outside the scope of building a company. There are probably only 1,000 people in the world qualified to do it. You now have to think about security, node communication, scalability, proof of work/stake/burn/space, regulatory compliance, stability, bitrot, etc.

- There are already lots of effective ways to reward and incentivize early adopters. For example, having a short twitter handle is a great benefit of being an early twitter user. For paid services you can offer lock-ins where you get a cheaper plan for many years. Many services have waitlists and reward the most beneficial users (perhaps those that share on social media) with earlier access. Kickstarter has also raised billions of dollars for unproven ideas.

- It confuses where the value is. Are customers using your product because they like it (and thus are willing to pay) or because they hope that everyone else will use it and their tokens will become valuable? The former is the foundation for a lasting enterprise, and the latter is how you create a house of cards. Tokens can encourage founders to go after the wrong customers.