時間序列--殘差分析

殘差=y-yhat

一般我們就停止在這裡了

但是如果殘差表現的有某種形式,代表我們的模型需要進一步改進,如果殘差表現的雜亂無章,代表確實沒什麼別的資訊好提取了

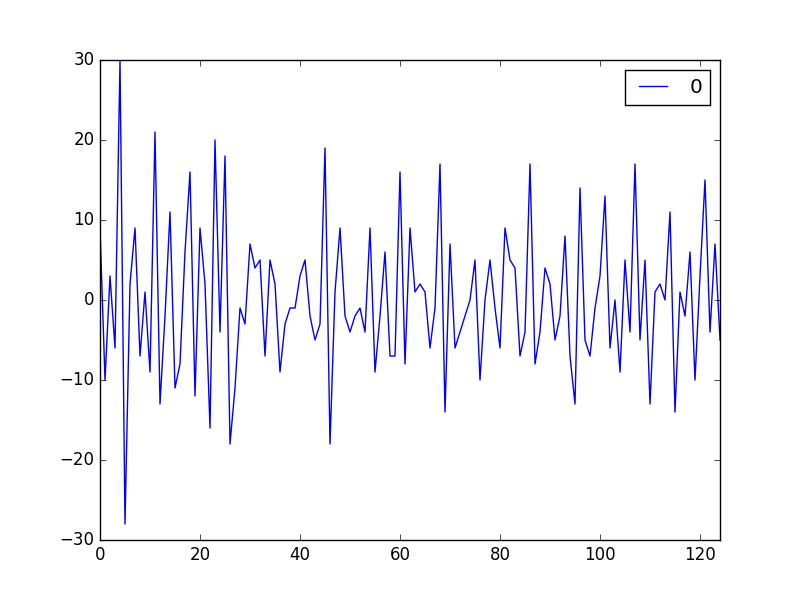

現在用最naive的model--上一個時間的值=yhat看看殘差表現吧

關於殘差,可以看我的另一篇文章https://mp.csdn.net/postedit/82989567

from pandas import Series from pandas import DataFrame from pandas import concat series = Series.from_csv('daily-total-female-births.csv', header=0) # create lagged dataset values = DataFrame(series.values) dataframe = concat([values.shift(1), values], axis=1) dataframe.columns = ['t-1', 't+1'] # split into train and test sets X = dataframe.values train_size = int(len(X) * 0.66) train, test = X[1:train_size], X[train_size:] train_X, train_y = train[:,0], train[:,1] test_X, test_y = test[:,0], test[:,1] # persistence model predictions = [x for x in test_X] # calculate residuals residuals = [test_y[i]-predictions[i] for i in range(len(predictions))] residuals = DataFrame(residuals) print(residuals.head()) residuals.plot() pyplot.show()

殘差表現如下:

現在看看基本資訊

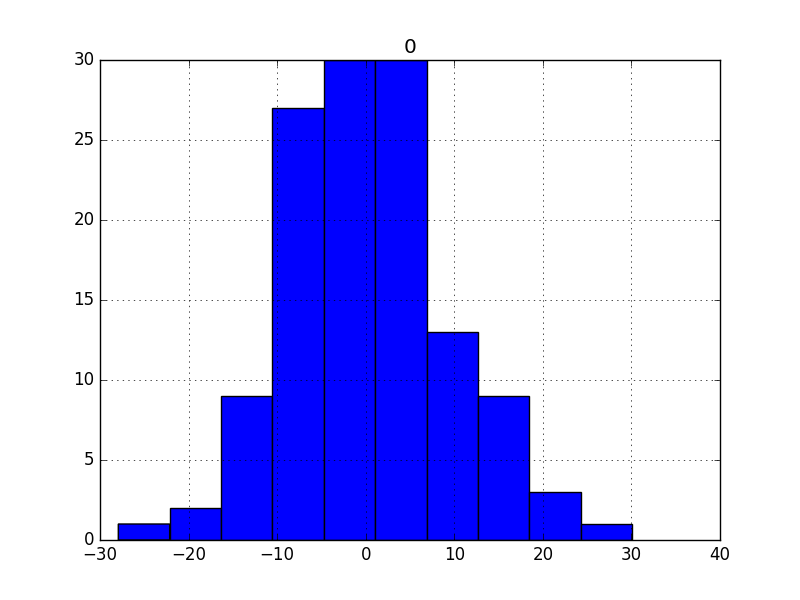

1.均值--越接近0越好

A value close to zero suggests no bias in the forecasts, whereas positive and negative values suggest a positive or negative bias in the forecasts made.

print(residuals.describe())

結果如下

count 125.000000

mean 0.064000

std 9.187776

min -28.000000

25% -6.000000

50% -1.000000

75% 5.000000

max 30.000000

mean和0還是有點差距

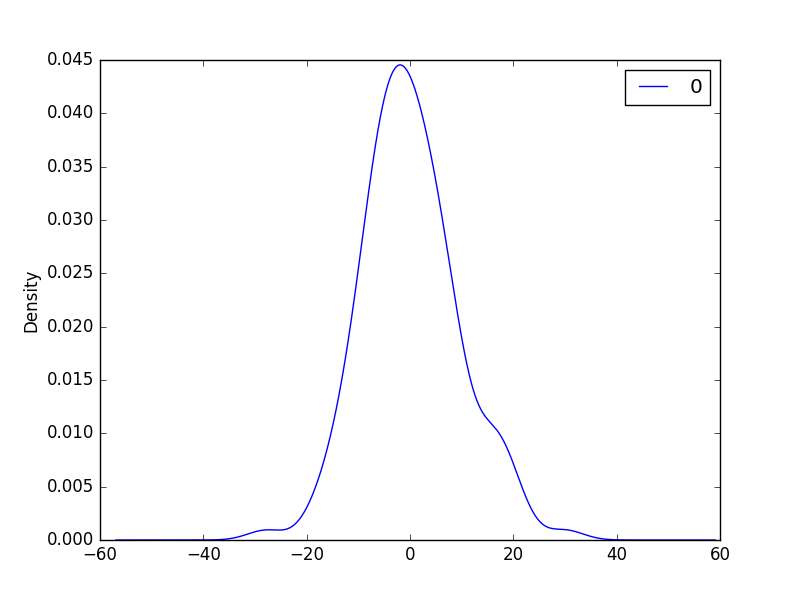

2.直方圖密度圖about殘差

我們希望殘差分佈越接近正太越好

If the plot showed a distribution that was distinctly non-Gaussian, it would suggest that assumptions made by the modeling process were perhaps incorrect and that a different modeling method may be required.

A large skew may suggest the opportunity for performing a transform to the data prior to modeling, such as taking the log or square root.

# histogram plot

residuals.hist()

pyplot.show()

# density plot

residuals.plot(kind='kde')

pyplot.show()

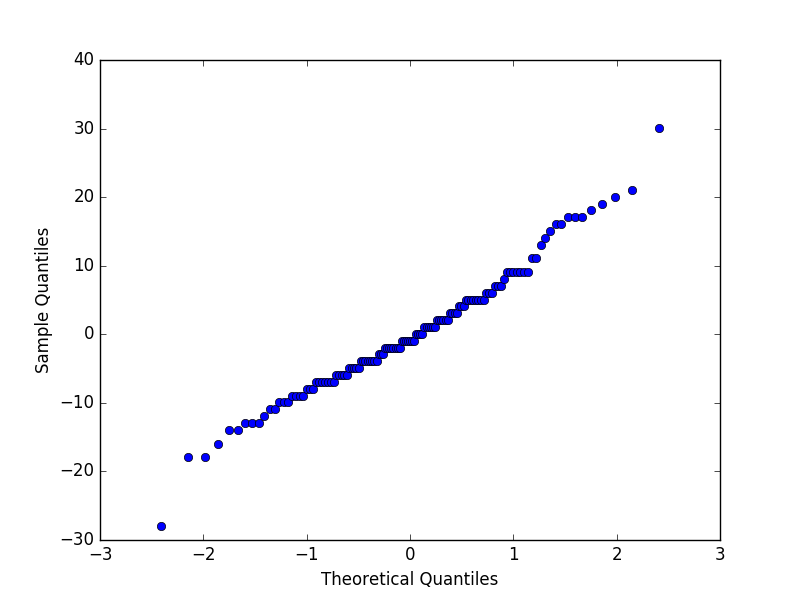

3.QQ圖檢驗正太更快速的方式

from pandas import Series

from pandas import DataFrame

from pandas import concat

from matplotlib import pyplot

import numpy

from statsmodels.graphics.gofplots import qqplot

series = Series.from_csv('daily-total-female-births.csv', header=0)

# create lagged dataset

values = DataFrame(series.values)

dataframe = concat([values.shift(1), values], axis=1)

dataframe.columns = ['t-1', 't+1']

# split into train and test sets

X = dataframe.values

train_size = int(len(X) * 0.66)

train, test = X[1:train_size], X[train_size:]

train_X, train_y = train[:,0], train[:,1]

test_X, test_y = test[:,0], test[:,1]

# persistence model

predictions = [(x-0.064000) for x in test_X]

# calculate residuals

residuals = [test_y[i]-predictions[i] for i in range(len(predictions))]

residuals = numpy.array(residuals)

qqplot(residuals)

pyplot.show()

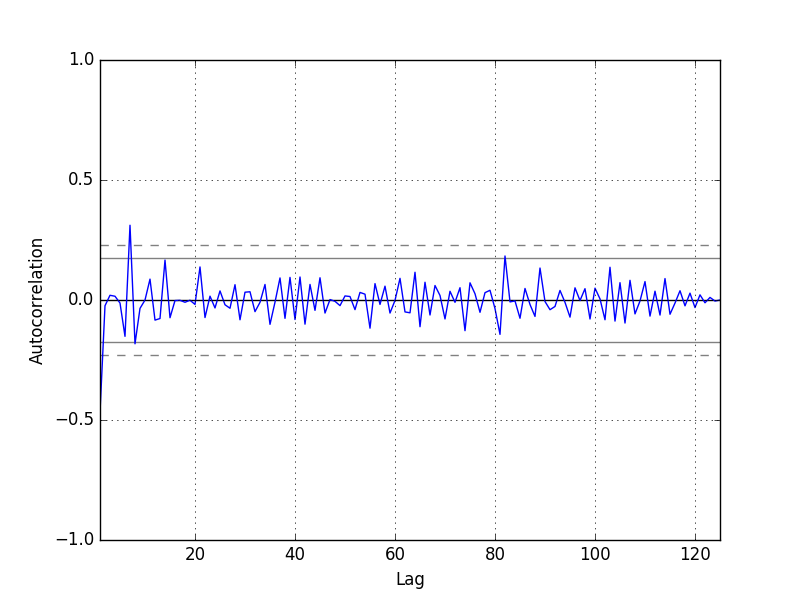

4.自迴歸圖

殘差的自迴歸越小越好!

We do not see an obvious autocorrelation trend across the plot. There may be some positive autocorrelation worthy of further investigation at lag 7 that seems significant.

https://machinelearningmastery.com/visualize-time-series-residual-forecast-errors-with-python/