Congress on the Blockchain

Just as the cryptocurrency markets began showing signs of recovery in early September, 2018, Congressman Tom Emmer announced three pieces of pro-blockchain legislation to be introduced before Congress.

In the September 21st press release Congressman Emmer reveals that he was just named the new co-chair of the

Specifically, the legislation expresses support for the industry and development of these promising technologies in the United States, provides clarity to entities that never take control of consumer funds, and establishes a safe harbor for taxpayers with “forked” digital assets.

The United States should prioritize accelerating the development of blockchain technology and create an environment that enables the American private sector to lead on innovation and further growth, which is why I am introducing these bills. — Congressman Emmer

The legislation is presented in the following resolutions and bills:

Status of the Legislation

At the time of writing these items of legislation have not been voted on or signed into law. They are proposals from Congressman Emmer on behalf of the Congressional Blockchain Caucaus showing pro-blockchain support for existing challenges faced by blockchain developers and enthusiasts.

Resolutions vs. Bills

In the United States a bill is an item of legislation that is created by Congress and signed into law by the President. Bills may add to, remove, or change existing laws, appropriate money, and define domestic or foreign policy amidst other things. They are prefixed by “H. R.” when proposed by the House of Representatives.

A resolution, on the other hand, does not have the force of law (except a Joint Resolution, which is identical to a Bill) and is used for things like expressing the sentiment of the legislative body. Simple resolutions, such as the one proposed, are prefixed with “H. Res.”

Note that the Resolution and Bill numbers (their IDs) are not specified and left blank since they have only just been proposed.

Support for Digital Currencies and Blockchain Technology

Congressman Emmer’s first proposed legislation is a Resolution expressing positive sentiment and congressional support for digital currencies and blockchain technology.

The Understanding of the United States

Specifically, the resolution:

- Compares blockchain technology and its promise to the successful rise of the internet.

- Proposes that the aforementioned success of the internet was due in part to the “light-touch” approach of government regulation as it developed.

- It references the five principles for the Global Information Infrastructure (which are: “encouraging private investment, promoting competition, providing open access to networks and services for providers and users, creating a flexible regulatory environment to keep pace with technological and market developments, and ensuring universal service”).

- Acknowledges that blockchain technologies such as digital currencies/cryptocurrencies can enable transferring “value” between users.

- Hopes that in combination with mobile devices blockchain technology can assist underserved populaces with banking and financial services.

- Hopes in addition that blockchain can be used for more than just currencies, including decentralized identity, Internet of Things security, digital rights management (DRM).

- Hopes further that blockchain technology can implement more efficiently services such as insurance, energy, health care, and smart contracts (digital contracts with instant, self-executing business rules).

- Points out that the permanent nature of blockchain entries can aid governments to improve transparency and prevent fraud.

- Believes these features of blockchains can improve access to business development and capital while encouraging innovation.

- Acknowledges that foreign nations are already experimenting with blockchain technology to improve services to their citizens.

- Further acknowledges foreign nations are finding themselves the home of new blockchain companies unable to thrive in the U.S. regulatory environment.

- Nods towards blockchain also being used as methods of fundraising, including tokens, and though unsaid but by extension, Initial Coin Offerings (ICOs).

- Promotes an understanding that blockchain technology can handle a variety of different use cases, and is a foundation upon which other technologies and services can be built.

- Demonstrates that the U.S. government (through agencies like the General Services Administration and financial regulators) have been collaborating on exploring use cases for blockchain technology.

And Thus the United States is Resolved To…

Following these acknowledges, references, and explanations the following resolutions are made:

- The U.S. should prioritize blockchain technology in a responsible way that benefits consumers.

- The U.S. should make a blockchain-friendly environment both for developers/businesses and the blockchain networks themselves.

- U.S. Federal agencies should create a framework to support digital currencies and blockchain technology.

- The U.S. should avoid unnecessary restrictions on blockchain technology.

- The U.S. should NOT abandon its responsibility to prevent illicit/illegal use of blockchain technology (drugs, etc). Proposes the need for a consistent and “light-touch” legal framework.

- The U.S. recognizes the potential usage of blockchain technology and digital currencies for both the public and private sectors.

The Resolution in Summary

Overall the resolution acknowledges the tremendous potential of both digital currencies and the blockchain technologies they depend on. The Congressional Blockchain Caucus seems resolved to treat blockchain development in the same way the Internet itself was — with a light touch.

The resolution responsibly acknowledges the potential dark side of blockchain technologies and cites the need to bring together regulatory bodies to create a “predictable” legal framework under which development and users can flourish.

The tone is bright and hopeful, offering official support by the U.S. government for the development of blockchain technologies including support for the private sector.

Blockchain Regulatory Certainty Act

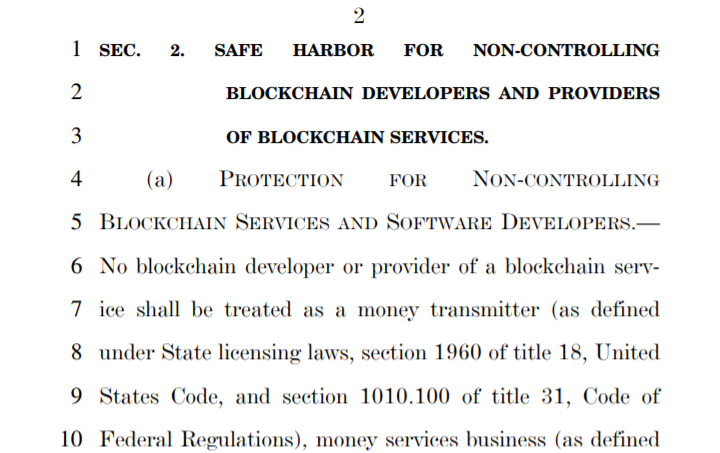

Congressman Emmer’s second piece of legislation, a bill, is intended “to provide a safe harbor from licensing and registration for certain non-controlling blockchain developers and providers of blockchain services.”

Protection for Non-Controlling Blockchain Services and Software Developers

Section 2(a) specifically prevents developers and service providers from being identified as “money transmitters” and prevents them from being required to undergo state or federal licensing or registration UNLESS they have control over a user’s digital currency.

As an example: developing a smart contract that automatically handles users’ funds (such as an automated escrow contract) should not be treated the same way as a cryptocurrency exchange.

Further: simply creating a cryptocurrency shouldn’t fall under regulation either. However, an Initial Coin Offering (ICO) WOULD fall under licensing and regulatory control given the holding and distribution of users’ funds.

In short, this bill ensures a predictable, non-interventionist stance, of the U.S. government towards blockchain developers and service providers who aren’t in control of funds.

Effect on Laws

Section 2(b) defines the effects of Section 2 on other laws:

- Any criminal laws will be unaffected by this bill, and thus the protections offered above do not override criminal law.

- Nothing in the bill is meant to expand or limit intellectual property laws.

- Nothing in the bill (really Section 2) can prevent states from enforcing their own laws that are consistent with Section 2. States are prevented from suing, making criminal, or imposing liability on things protected in this bill.

Legal Definitions for the Blockchain Environment

Section 2(c) provides legal definitions for key terms and ideas in blockchain development:

- “Blockchain Network”: mentions that consensus is required across a network without proprietary licensed software; specifically includes distributed ledgers

- “Blockchain Developer”: a person or business that makes, maintains, or spreads blockchain software, networks, or services

- “Blockchain Service”: anything that accesses a blockchain network

- “Control”: legal right/authority to spend digital currency (e.g. transactions)

- “Digital Currency”: a medium of exchange, or store of value, in a distributed ledger

The First Bill in Summary

The Blockchain Regulatory Certainty Act protects, at a federal level, the common cases for blockchain development both for software developers and service providers.

It prevents individual states from making their own regulations that would harm the average developer or service provider, while allowing for regulation and licensing of blockchain developers or services involved in controlling users’ funds (such as cryptocurrency exchanges).

This preserves the role of the U.S. Securities and Exchance Commission (SEC) and the Financial Crimes Enforcement Network (FinCEN) while, at a federal level, enforcing the protection of the U.S. blockchain environment.

This idea of a “Safe Harbor” is akin to how internet service providers (ISPs) can’t be held responsible for the actions of their users and act as a “service” — enshrining this concept of safe harbor is incredibly important for the blockchain environment.

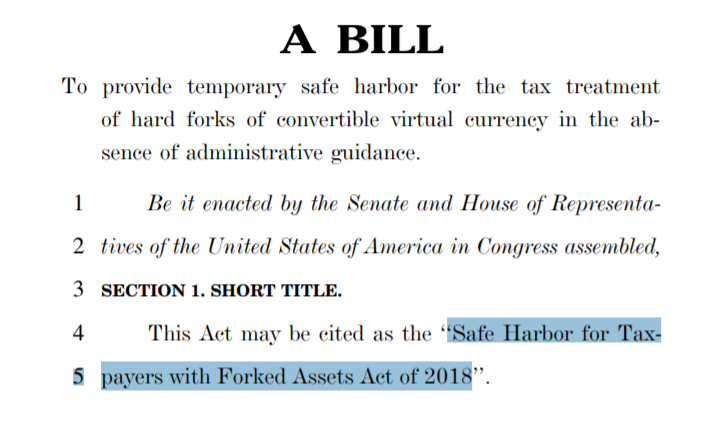

Safe Harbor for Tax-payers with Forked Assets Act of 2018

The second bill is designed to provide reasonable protections and tax guidance for handling “hard forks” of cryptocurrencies.

During a “hard fork”, such as the creation of Bitcoin Cash from Bitcoin, holders of the original coin suddenly have the same amount of new currency in the new “fork” — it’s a copy of the last state of the distributed ledger before the fork.

Why is this important? Current tax law treats cryptocurrencies as assets that, when mined, have a $0 cost-basis. That means if you happen to successfully mine some Bitcoin (at today’s price of $6,708.10) you would owe the government capital gains tax (treated as self-employed income) on the value of the coin when it was mined.

Now, if someone copies a cryptocurrency and you suddenly have the same balance in your wallet in the new one, do you owe the government money? How much? When? You weren’t even involved in the forking process (most likely) in the first place!

This bill addresses this all-too-common situation.

Understating and Under-reporting the Problem

Section 2(a) is concerned with a user who receives a forked virtual/digital currency.

2(a)(1) prevents penalties or additions from being assessed by the IRS for underpayment or understatement of taxes by a given taxpayer attempting to follow the tax code.

As a person who is not a tax lawyer specializing in blockchain technologies I cannot fully speak for the intent of the paragraph here. It seems, on the surface, to be acknowledging the situation in which a taxpayer receives a forked virtual currency at some point (either known or unknown to them), and once they make an effort to comply with the tax laws they can’t be penalized for not doing everything perfectly from the get-go.

This interpretation would make since given the ill and undefined nature of tax law guidance around forked virtual currencies. In short: you still have to pay taxes on any gain (including a forked virtual currency), but, with an understanding that the tax situation has historically been murky in this case, taxpayers should not be penalized for mistakes/errors in attempting to follow the tax code.

2(a)(2) follows the same logic as 2(a)(1) in regards to not penalizing failing to file the proper tax forms related to the forked cryptocurrency.

It seems that the idea is that the tax is still due and expected once identified but any misunderstandings, failings, or mistakes up to the point the taxpayer properly reports and pays taxes on the forked virtual currency (such as after actually selling it) will not be actioned.

Note: I am not a lawyer or CPA and this is not tax guidance!

Special Definitions We Need to Know

Applicable Period

The most important definition of the bill is the “applicable period” under which Section 2 operates. Thankfully, the definition is simple: it lasts from any moment before the bill is enacted until the Secretary (or other laws) fully define and legislate:

- The tax treatment of forked virtual currencies

- Rules for calculating and allocating the basis of forked virtual currencies

- Rules for calculating the fair market value of forked virtual currencies

- Rules for determining the holding period of forked virtual currencies

In other words, this bill creates a temporary safe harbor UNTIL actual legislation or guidance is created that defines the above issues. This protects all U.S. cryptocurrency users from the current ambiguous situation regarding forked virtual currencies.

Forked Convertible Virtual Currencies

The term “forked convertible virtual currencies” is given a legal definition of any virtual currency given to a taxpayer as the result of a hard fork.

A “convertible virtual currency” is given the legal definition of any digital representation of value that functions as a medium of exchange, doesn’t have status as legal tender, and has an equivalent value to legal tender.

A “hard fork” is given the legal definition of a material change to a digital ledger upon which a virtual currency is based that results in an independent digital ledger.

“Constructive receipt” includes actual receipt or the right to receipt (such as having ownership of Bitcoin inside of an exchange, and thus being entitled to equivalent Bitcoin Cash at the time of the fork) of a convertible virtual currency.

The Hard Fork Safe Harbor in Summary

This bill properly acknowledges the ambiguous tax situation involving hard forked digital currencies that currently plagues the booming cryptocurrency environment.

It protects users from this tax situation by (softly) deferring requirements to report to the government the receipt of hard forked virtual currencies until proper legislation and guidance is enacted into law.

This safe harbor goes on to provide legal definition to these relatively new technical concepts that have resulted from the explosive growth and adoption of cryptocurrencies.

A technical nitpick of the bill would be a fix for Section 2(b)(2)(C) in which “digital ledger” is used rather than “distributed ledger”, the latter being the consistent term involving blockchain networks.

Conclusion

The simple resolution is a much-needed, public, pro-blockchain sentiment of support by Congress. It addresses the use cases for blockchain, acknowledges the race amidst foreign nations to support development for private and public sectors, and proposes regulatory and financial support for blockchain technology including digital currencie.

The first bill protects average developers and service providers from burdensome regulatory and licensing requirements not needed by those not in direct control of users’ funds.

Additionally, since cryptocurrency users most often have no control over whether a virtual currency they use will be hard forked by some future party it makes perfect sense to shift the burden towards the government to better define legislation for these events before penalizing and suppressing cryptocurrency usage through ambiguous tax law.

Overall, these bills are common sense and will encourage further blockchain development in the United States.